How to Pay for Long-Term Care: 8 Strategies

Long-term care planning—if not now, when?

Two big questions loom as the American population comes of age for long-term care—How do I plan for it? Can I afford it?

When it comes to planning for a safe and secure retirement, long-term care (LTC) can be a confusing and unaddressed challenge to many families’ financial security. Some of the hesitancy can be pinned to human nature—we don’t like to think about the unpleasant possibility of needing help being fed, bathed or using the bathroom. Some might think it won’t happen to them. Others can’t think that far down the road.

Some additional hurdles include:

- Underestimating the cost of care

- Knowing the cost and not comprehending how to pay for care

- Mistakenly assuming Medicare and health insurance will cover LTC needs

- Traditional long-term care insurance has had a bad rap, due in part to significant premium hikes on early polices that were initially mispriced and delivered inconsistent benefits

- Some find it problematic to pay a great deal of money for something they may never use

Planning can help

While it might sound simplistic, handling these issues starts with a conversation to get the ball rolling. The act of discussing and planning can help alleviate the emotional, financial and physical stress related to LTC. According to a 2018 study by Genworth, of those who prepared, 66% wished they had taken steps to plan sooner.

In those situations where LTC was needed, 84% of caregivers and 75% of recipients report they would have “done things differently.” Without a plan, you may have to make in-the-moment and subpar decisions to help a loved one. Crisis planning can end poorly.

How to pay for LTC

The good news is that planning and products have evolved. Let’s dig into what can be done today to help ease the worry and challenges posed by growing older.

1. Medicare vs. Medicaid

Several strategies are at your disposal to help cover costs associated with LTC.

But not Medicare. Most people believe their LTC needs will be covered by Medicare. Medicare will pay for short stays in skilled nursing facilities that provide rehab or therapy services after a hospital stay. However, Medicare does not cover long-term care.

In contrast, Medicaid covers long-term care costs at home or in a skilled nursing facility. In fact, Medicaid is the primary payer for long-term care services. The biggest issue is that many people who need long-term care never qualify for Medicaid assistance. Here’s why:

- Income thresholds. Individuals must have limited income and assets to qualify. If one is above those thresholds, current assets must be “spent down” before utilizing Medicaid.

- Lookback period. There is a lookback period when assessing eligibility. In most cases, a review of financial records, going back five years, will seek to uncover whether assets were sold or given away to meet your state’s asset limit.

- Medicaid pending. Even if an individual qualifies, there might be a period called “Medicaid pending” where benefits have been denied or the recipient not approved. This can be quite stressful, especially if immediate care is needed. Not all facilities will accept a person who is in pending status.

- Bed availability. Additionally, a bed may not be available at a preferred facility.

2. Self-funded long-term care

Perhaps an individual cannot qualify for traditional long-term care insurance (LTCI) due to existing health issues. In this situation, they will have to use savings or investments to pay for care out of pocket and should set money aside for two to three years of LTC. Planning early is key to success. The best advice may be to live under one’s means and save more.

The downside to this approach is not knowing how many years of care may be needed. Alzheimer’s has an average life expectancy after diagnosis of eight to ten years, according to the Alzheimer’s Research and Prevention Foundation. The funds to cover five years in a facility may be available but would deplete all assets in year six with nothing left for beneficiaries.

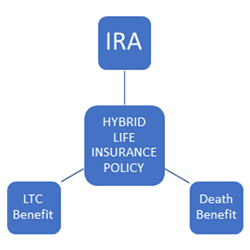

3. Use pre-tax savings, like an IRA

Another strategy designates pre-tax savings (IRA) to purchase LTC protection. Retirement assets can be surprisingly substantial and a good source for LTC needs. Some things to think about:

Purchasing a hybrid life insurance policy with proceeds from an IRA means if long-term care is not needed, the death benefit flows to the estate tax-free.

- Tax change alert: The SECURE Act of 2019 instituted an important change to lifetime “stretch” IRA options. Previously, non-spouse beneficiaries were allowed to stretch their required minimum distributions (RMDs) over their life expectancies, thereby extending tax implications. The SECURE Act now requires non-spouse beneficiaries to take all distributions within a 10-year period following the death of the retirement account owner. This compels the beneficiary to pay taxes sooner.

- As a solution, the IRA owner could purchase a hybrid life insurance policy with proceeds from the IRA and gain LTC coverage with a death benefit. If long-term care is not needed, the death benefit flows to the estate tax free.

- To avoid the 10% penalty for those under 59½, consider using Rule 72(t) distributions to fund LTC premiums. This rule allows penalty-free withdrawals from IRAs and other tax-advantaged accounts and requires a specific distribution schedule, which will be taxed as ordinary income. There are some restrictions around this approach, but for those who are a year or two away from age 59½, it may be useful.

4. Explore Roth IRAs and backdoor Roth IRAs

Assets pulled from a traditional IRAs are taxed as ordinary income. Luckily Roth IRAs are funded with after-tax monies, and feature tax-free growth, tax-free withdrawals and no RMDs. Earmarking a Roth for LTC costs or premiums may be an excellent strategy.

Higher earners will also benefit by using what is called a backdoor Roth IRA. This is an IRS-permitted method allowing one to fund a Roth IRA even if income is higher than IRS limits for standard Roth contributions or conversions.

Funds can be used to pay for LTC costs or pay premiums for coverage. Please note—taxes must be paid on monies converted to a backdoor Roth IRA and it will likely count as income, possibly pushing one into a higher tax bracket.

It is always helpful to speak to a tax professional to assess every individual’s unique situation.

5. Mine your health savings accounts

A health savings account (HAS) is a hidden jewel in your LTC and retirement planning arsenal. The approach is simple, effective and tax-advantaged.

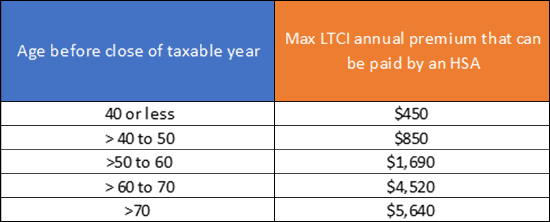

Figure 1: 2021 Amount of HSA Assets That Can Be Used to Cover Long-Term Care Insurance

Source: Internal Revenue Service

- Contributions to an HSA reduce annual taxable income and grow tax deferred until monies are used to cover eligible health care expenses.

- HSA withdrawals for medical expenses and LTCI are tax-free when they meet certain guidelines. Based on age, one can use HSA monies tax-free to pay LTCI premiums (see Figure 1). To make this work, the long-term care policy must only cover long-term care services. Most LTCI policies qualify.

- After age 65 the money can be used for absolutely anything without penalty (although ordinary income taxes will be due on withdrawals). While there are annual contribution limits, there is no maximum accumulation limit for an HSA. For example, 2022 Annual Contribution Limits are: $3,650 self only, $7,300 family contribution limit plus a $1,000 catch-up provision for those 55+.

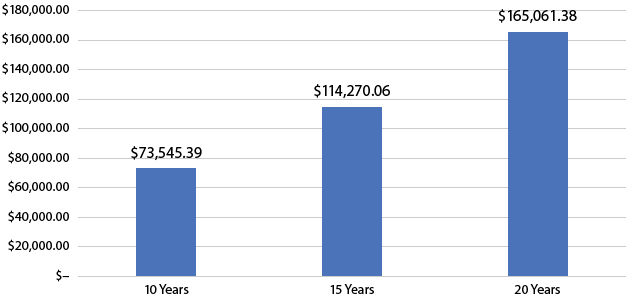

As Figure 2 illustrates, contributing to an HSA over time can result in a substantial balance.

Figure 2: Growth of HSA Dollars$500/month at 3% annual growth rate

Source: Internal Revenue Service

6. Leverage your home: Reverse mortgage

Individuals wishing to cover long-term care costs can leverage perhaps their greatest asset, their home, to pay for LTC expenses or an LTCI policy. The first option to take a look at is the reverse mortgage. For those 62 and older, the lender makes a loan in a lump sum, monthly installments or as a line of credit for the homeowner. The loan is typically paid back with interest when the home is sold. For seniors, there is some comfort in knowing that the Home Equity Conversion Mortgage (HECM) is insured by the U.S. Federal Government. What you need to know:

- The homeowner can never be forced out of their home.

- The loan is not counted as income and does not affect Medicare or Social Security benefits. It may, however, impact Medicaid eligibility.

- There are no restrictions on how the money can be used.

- Loans can fund home care, adult day care or premiums for LTC coverage. One can use the proceeds to make their home safer and accessible, allowing for an indefinite stay in their residence.

- If one passes away, the remaining spouse can still live in the home.

- This option may not be the best solution if both spouses need care and enter a facility. Reverse mortgages are due when the last borrower dies or moves out.

- When the home is sold to repay the mortgage, if the proceeds of the sale are less than the mortgage, the lender must take the loss and cannot go after other assets of the homeowner or homeowner’s estate. In most cases, the homeowner cannot pass the property to heirs.

There are some important considerations when using a reverse mortgage for LTC. The lender will want to make sure the homeowner is financially capable of maintaining their home. In some circumstances the lender will require funds set aside to cover these costs.

The borrower can live outside the home (think nursing home) for up to 12 months before the loan is due. This could be an issue if one spouse is in a nursing home and the other dies while still living in the house. The loan is due in one year.

Finally, reverse mortgage closing costs can be as high at 8% of the loan amount—significantly higher than a home equity line of credit. Certainly, some things to digest when weighing one’s options.

7. Leverage your home: Home equity line of credit

A home equity line of credit, or HELOC, can be a great alternative to a reverse mortgage and is a quick and easy way to access money for care or insurance. Loans based on equity in one’s home may be cheaper than reverse mortgages, which tend to have higher closing costs. Borrowers may be able to access up to 80% of their home’s equity. Additionally, HELOCs are extremely flexible as it relates to withdrawals and payback periods. To top it off, interest on the loan can be tax deductible in the year the interest is paid.

Furthermore, there is no requirement for the homeowner to maintain residence while the loan is in place. In this scenario, a HELOC has a clear advantage over a reverse mortgage. And, what if the person needs to sell their home to move into a facility? A HELOC can provide an excellent bridge strategy covering costs and expenses until the home is sold.

A HELOC is not without some downside. If the homeowner is unable to repay the loan, the lender could foreclose on the property. In addition, while rare, a lender could freeze the loan without ample warning.

8. Existing life insurance

There are a few ways an existing life insurance policy can help fund LTC. Individuals may have traditional life insurance policies that could be sold to a life settlement company. Proceeds will depend on the age and health status of the policyholder. Some life insurance policies offer “accelerated benefits” in the form of a cash advance against the death benefit. Some insurance carriers may make an accelerated benefit available even if it is not in the contract. Either way, the upside may outweigh any reduction in death benefit for beneficiaries.

Products for consideration

Now that we’ve reviewed how to pay for care, here are several product options that should be considered.

- Traditional long-term care insurance—A specific insurance policy that offers comprehensive LTC coverage. The policy helps cover the costs of care in a person’s home or a facility due to a chronic medical or cognitive condition.

- Life insurance with LTC benefit—Also called “hybrids” these life insurance policies feature both a death and LTC benefit. If the LTC benefit goes unused, the death benefit is available for the beneficiaries.

- Annuities with LTC benefits—Two annuity categories are worthy of review—long-term care annuities and fixed indexed annuities (FIAs) with LTC benefits. The products feature an enhanced pool of money that can be used for care once triggered.

Let’s finish where we started—if not now, when?

Thinking about long-term care can be difficult but as they say, “necessity is the mother of invention.” Challenges along the way have led to innovations in recent years and there’s reason to feel hopeful about one’s ability to address the long-term care conundrum.

Start small. An initial conversation to get the ball rolling can go a long way. Next, integrate the discussion with the financial planning process, just as one would tackle saving for retirement or income in retirement. The risks and costs of long-term care are among the most important considerations—fortunately, there are an array of solid tactics and solutions available. Given the enormous potential impact on assets, we can all benefit from the dialogue.

Please be sure to discuss unique tax situations with a CPA or qualified tax professional.